VAT Compliance Solutions | Guide to Dutch Fiscal Representation

Empowering cross-border businesses to establish compliantly in the Netherlands, optimize VAT cash flow, and grow across the EU.

What is a Dutch fiscal representative?

A foreign business may appoint a Dutch local tax company as its fiscal representative to fulfill VAT-related administrative and compliance obligations in the Netherlands on its behalf. In certain circumstances, appointing a fiscal representative is a legal requirement — for example, when a foreign business intends to apply for the Dutch Article 23 import VAT deferment license.

The fiscal representative handles VAT matters in the Netherlands on behalf of the foreign business, including but not limited to:

Taxable business activities within the Netherlands

Intra-community acquisitions, supplies, and stock transfers

Imports from non-EU countries and exports to non-EU countries

The fiscal representative bears joint legal liability for the VAT owed by the foreign business to the Dutch tax authority, as well as for related compliance operations. Their specific responsibilities include: periodically reviewing the compliance of VAT-related data and documentation maintained by the foreign business, and filing the VAT Return and EC Sales Listing on its behalf, as well as submitting the Intrastat Declaration to Statistics Netherlands (CBS) where applicable.

What is the Article 23 import VAT deferment license?

The Article 23 import VAT deferment license is a key benefit of GFR in the Netherlands, which allows import VAT to be deferred to the VAT return rather than paid at the point of importation (for reporting purposes only; no actual tax payment or refund is involved) — offering a significant cash flow advantage unique to the Dutch system.

To act as a fiscal representative, a valid license is required. There are two types:

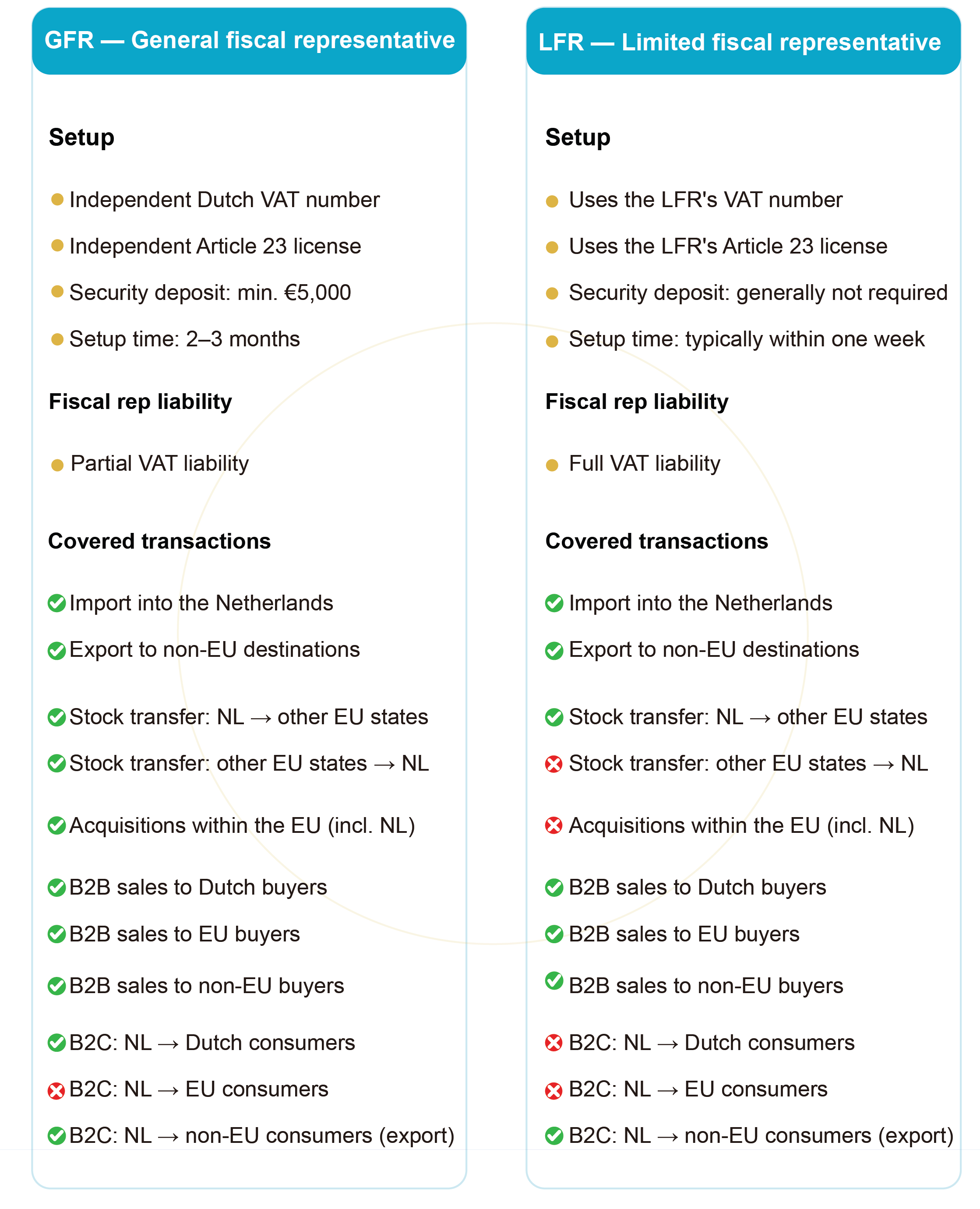

General fiscal representative (GFR) & Limited fiscal representative (LFR)

The two differ fundamentally in their scope of coverage and liability structure.

Note: 1) All entries above are based on goods supply scenarios. 2) LFR coverage reflects both Dutch VAT regulations and Augmar's internal business policy. 3) The listed transactions represent primary routine taxable activities and do not constitute an exhaustive list.

How to handle intra-EU B2C deliveries compliantly?

Register for OSS (One Stop Shop)

What is OSS?

OSS (One Stop Shop) is an intra-EU B2C VAT simplification scheme that allows businesses to register for OSS in a single EU member state and report all cross-border B2C sales across the EU through a single quarterly OSS VAT return. Rather than registering for VAT separately in each EU member state where sales are made, businesses can manage all their intra-EU B2C VAT obligations through one central registration.

Want to learn more?

Contact us today — we'll craft a logistics and tax solution tailored to your business.

Free initial consultation